The fight between EcoCash and their regulator, the Reserve Bank of Zimbabwe is revealing if nothing more. Of course the current episode started with a directive from RBZ instructing EcoCash to freeze agent accounts that transact above ZW$100,000. EcoCash went to court seeking an urgent reversal, the RBZ responded and now we are here.

Reading the EcoCash lines and between them

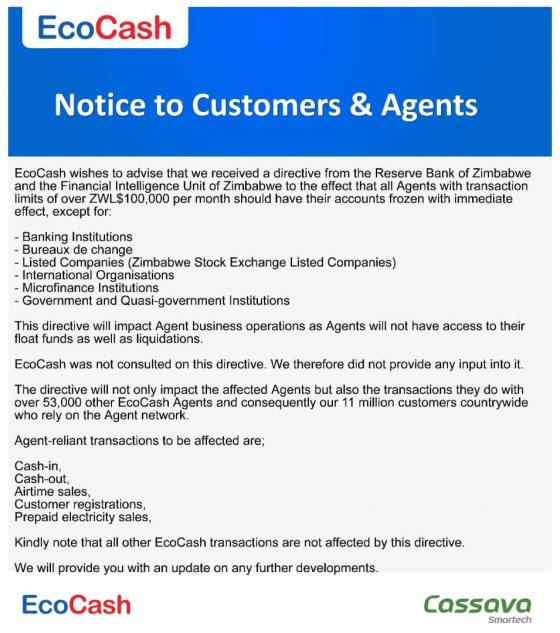

The Econet group knows how to play in two arenas very well: the arena of the courtroom and the arena of public opinion. When EcoCash was served with the directive they didn’t hesitate to indite RBZ in the public opinion courtroom. They presented their issue:

11 million

EcoCash mentions 11 million customers in the above notice to the public and several times in the papers they submitted to the High Court. For example, EcoCash’s lawyer states this:

The directive hurts the -Zirnbabviiean population and the Applicant’s business. There is a seasonable apprehension of financial loss by 11 million Zimbabweans

This is not a very truthful position. EcoCash launched in 2011 and since then they have cumulatively registered about 11 million customers. That doesn’t mean in any way that they have 11 million customers that are prejudiced by the RBZ directive.

First, as at December last year the total number of active mobile money subscribers in Zimbabwe was 6.5 million. Active subscribers are defined as all subscribers that have performed at least one transaction in the 90 days prior. Yes, EcoCash has the lion’s share of this number but it’s not 11 million Zimbabweans as stated. Of course there are some subscribers that fall out of that 90 day window that are really EcoCash customers but the fact of the matter is that 11 million customers is a stretch. A good number of those subscribers already died for example.

Secondly, the RBZ did not say all agents must be shut down. We will come back to this point later. For now we will just acknowledge that EcoCash cannot claim that all their subscribers are affected by this directive when just a fraction of their agents are affected.

Thirdly, everyone knows that not much cashing in and cashing out is happening. No one is using cash that much in this country. Agents mainly exist to facilitate cash liquidation onto and off the platform. This is not happening anymore. In fact, the fact that so many cash in and out transactions are still happening is evidence that the RBZ suspicions are legitimate.

Generally no cash is changing hands when cashing in and out is happening except for forex. This is a public secret. It therefore means very few of EcoCash’s subscribers will have legitimate transactions affected by the directive. Yes, EcoCash is talking about how agents facilitate payment of bills etc. How do agents help customers pay bills? Subscribers can do these functions all by themselves.

O level math will tell you that the probability of any subscriber being affected is very low: Probality that agent transacted above $100k X Probability that customer needs to legitimately do a cash in/out.

Throwing around the 11 million number is EcoCash’s way of courting public sympathy and an attempt to catch the court snoozing.

53 thousand

Another number EcoCash has been throwing around at every turn is 53,000 agents. The total number of EcoCash agents is irrelevant because the RBZ did not say all agent accounts must be frozen. The number EcoCash should be furnishing the court and public sympathisers is the number of agents that transact above the ZW$100,000 per month.

In his affidavit to the High Court, Eddie Chibi, the CEO of Cassava Smartech (EcoCash’s parent) uses a lot of words to try to mask the fact that very few agents are affected:

The institutions that have transactional values of above ZW$100,000.00 per month but are exempted from suspension and freezing under the directive of 4 May 2020 only constitute 4% of the Respondent’s Agent base of those values of transactions. They are mostly located in urban areas and the rural people who form 65% of the country’s population will not be able to access service provided by these Agents. The Applicant and its customers will be severely prejudiced because 96% of the Agents will be disentitled from providing the Applicant’s services. The exempted Agents will not be able to fill the gap that will be created by the Agents whose accounts would be suspended and frozen in terms of the directive issued on 4 May 2020. As a result, the Applicant will suffer irreparable harm because it will not have enough Agents to offer its services. This will also harm the Applicant’s reputation and goodwill because it will not be able to provide services to all its customers as it usually does.

Those words are designed to lead to a false inference. It’s not 4% of agents that will be able to operate, it’s 4% of agents that meet the RBZ criteria. The exempted institutions are not too many (banks, listed companies, international organisations and government departments) we can infer that affected agents are somewhere between 2,000 and 5,000. Most likely closer to 2,000 and it’s possible they are even less than that number.

If the number was significant, EcoCash would have shouted it from the roof tops. By the way the part about how all exempted agents are in urban areas prejudicing rural folk is nonsense. How many rural agents are transacting above $100k? How many customers does EcoCash have in the rural areas in the first place? That line is meant to draw false conclusions.

A substantial weight of the EcoCash argument is based on the number of agents and how their absence affects 11 million Zimbabweans. This is sad because I believe EcoCash is right to challenge the RBZ directive. It is an irrational order that punishes people for nothing beyond the fact that they transact above a certain threshold. This is no different from being arrested for earning whatever salary you earn.

It’s sad that EcoCash chose to lace a legitimate challenge with some silly manipulation of the language and facts. Such action only detracts the conversation from the important points and we start pointing out these inconsistencies. For example, in his High Court affidavit, the RBZ Governor, John Mangudya called them out for not furnishing the court with the ratio of agents viz the directive under dispute. Part of his affidavit says:

It is telling that the applicant has not been candid with this Honourable Court by setting out in detail the so-called affected agents, their identity and their KYC documentation. This is because the applicant has not been complying with the law and is unable to produce this information. Without the information the applicant has not made out a case for an interdict

It’s not just EcoCash acting funny:

The RBZ not answering the question posed

The central bank is also doing its fair share of trying to twist the debate towards a different plane.

Strategy: attack EcoCash

The RBZ’s court strategy seems to be to just throw mud all over the place and attack EcoCash. The issue under contention at the High Court is whether the directive the Reserve Bank issued is a legitimate directive. I think it is beyond doubt that the directive doesn’t satisfy that standard.

Imagine POTRAZ (the telecoms regulator) one day waking up and instructing mobile network operators to switch off all subscribers who spend more than 10 hours on WhatsApp per month because WhatsApp is being abused to spread fake news. This is the same thing that Mangudya’s institution has done. A business is being treated like a criminal just based on volume of transactions.

EcoCash has questions to answer but…

Get me right, I am not saying that issues raised by Mangudya in his affidavit are not important. EcoCash has to satisfactorily answer the question of whether they are printing money or deliberately causing delays in transaction settling so as to divert money and spin it on the black market. However, the RBZ could have indited EcoCash as an institution instead of going after EcoCash customers in a blanket manner.

The Governor said:

The applicant can only operate the payment systems in a lawful way. Operating the payment systems unlawfully through a Ponzi Scheme and shadow banking amounts to a violation of the law and does not give rise to any rights that the applicant can seek to enforce in the manner sought

If there are such issues at EcoCash then why not bring EcoCash to book not EcoCash agents.

Added to that, the RBZ has not been following through to investigate suspicious transactions flagged by EcoCash. How then can they punish collective groups when they will not be bothered to investigate obviously suspicious transactions?

The bigger problem

Our central bank and our government will point to anyone else and everyone else before they admit that we are in this mess because of them. Are there unscrupulous agents on the EcoCash platform? Yes there are but why does opportunity exist for them in the first place? Even if EcoCash is shut down completely today, will we not see people at street corners changing currency? Will we not see the local currency in free fall? So Governor Mangudya the problem is not EcoCash, we have a bigger problem.

No noise please

I have to wrap this up by saying EcoCash and RBZ please ask and answer the right questions to each other before the courts and in the public. Don’t try to confuse us with noise.

What’s your take?