Back in 2011 when EcoCash was introduced, I don’t think any of us envisioned how ubiquitous the payments platform would become close to a decade later. In fact, our article covering the EcoCash launch 8 years ago only viewed the mobile money service as a peer to peer platform:

EcoCash will work almost exactly like Safaricom’s M-Pesa. Consumers will be able to deposit cash into their EcoCash accounts through registered agents. The money in the EcoCash account can be transferred to any mobile subscriber in Zimbabwe, regardless of the mobile network.

Recipients will simply need to visit a registered agent to redeem their cash. A big focus of the platform is bridging the rural-urban divide where remittances are concerned.

Whilst we acknowledged that merchants would accept EcoCash we didn’t gauge how impactful the platform would be. For a significant number of people (myself included) the mobile money platform is their first encounter with a financial service.

Considering how long EcoCash has been around for, we wondered if EcoCash is now better or at least more convenient than a regular bank. We’ll compare a number of scenarios/use cases and attempt to come up with a conclusion as to what’s better.

Ease of setting up…

First things first, how easy is it to get in the door for customers of either service?

Signing up for an EcoCash account is a fairly simple process –you just need to fill out a form at an Econet shop/agent, have an active SIM with any of the 3 MNOs and voila you’re done.

Opening a bank account, on the other hand, is more complex. First of all, for some banks, you have to be above 18 years of age and you’ll need more details which include current proof of residency, proof of income along with some passport-sized photos (in some cases).

The rigorous KYC process for opening a bank account is one of the main reasons why adoption of mobile money has been so widespread over the better part of the decade. The process of opening an EcoCash account is also much easier simply due to the fact that their agent system has far more reach than the bank’s branch networks.

More recently it’s become easier to open lite accounts with banks like Steward Bank which have less strenuous sign-up processes and have also adopted an agent system but in most cases setting up a mobile money account is easier than a bank account.

Swipe 0 – 1 EcoCash

Speed

You haven’t lived a full life if you haven’t heard the cliché “Time is money” and the question becomes what’s quicker, EcoCash or Swiping?

We performed 3 transactions with each payment method and averaged the time it took to complete transactions in a shop:

- Swiping took 19 seconds

- EcoCash took 54 seconds

If you’re impatient, you might as well ditch EcoCash and stick to your bank card. EcoCash transactions take so much time because of the multiple steps it takes to actually initiate and complete the transaction – from entering your number in the POS machine/ entering the merchant number > then amount and then waiting for the prompt to pop up on your phone. Swiping is much quicker because there are considerably fewer steps – i.e swiping the card and entering the pin.

OneMoney has eradicated this problem by allowing you to enter your number and then the pin directly into the POS machine, but unfortunately, that’s not widespread and will probably still be a slower than plain ol’ swipin’.

Swipe 1-1 EcoCash

Convenience

One of the factors that people love about EcoCash is the fact that it lives on a device you ALWAYS have with you – your mobile phone.

This makes it extremely convenient since it’s next to impossible to forget your phone as you would a bank card. Because most people have wallets/purses and are mandated to move around with their ID, the convenience doesn’t offer a night and day difference since you probably already move with your wallet – carrying a card won’t be irritating.

On days that you decide to move without the purse, however, you’ll still have your phone which means EcoCash is wherever you’re 9 out of 10 times. Heck, even if you’re going for a run you’re more likely to have your phone with you than you’re to have your wallet.

Swipe 1-2 EcoCash

Distribution & Reach

Mobile money takes this one with little to debate about. The 47 000 strong mobile money agent network outnumbers the 549 ATMs countrywide. Whilst the 20 000 merchants on the EcoCash platform are heavily outnumbered by the 107 067 POS machines – once you consider the number of POS machines you find in one shop and the fact that a lot of traders aren’t registered on EcoCash as merchants, it becomes clear just how much of an advantage EcoCash has in terms of reach and distribution.

For traders in certain areas, acquiring POS machines is expensive and the expense isn’t worth it since the people in these areas don’t have bank accounts.

One of the reasons mobile money is a revolutionary technology is that the barrier of entry for both traders and buyers (and those using it for P2P) is incredibly low when compared to banks.

Swipe 1-3 EcoCash

Uptime

Whilst the Mid-Term Monetary Policy statement of 2019 makes mention of the uptime of financial payment systems – it doesn’t further break it down to show how the banking sector fared on its own vs mobile money.

In terms of operational reliability, the payment system in the country achieved an average uptime of over 95% during the period under review. The Bank continued to maintain a strong focus on ensuring the resilience of the payment system infrastructure against cyber threats.

What’s become clear however is that due to the fact that people who have bank accounts are fragmented across 13+ banking institutions any downtime suffered by individual banks will be much less impactful than the effect of EcoCash downtime. Because of EcoCash’s monopoly on the mobile money market – downtime basically brings the nation to a halt which isn’t the case with any banking institution in isolation.

Swipe 2-3 EcoCash

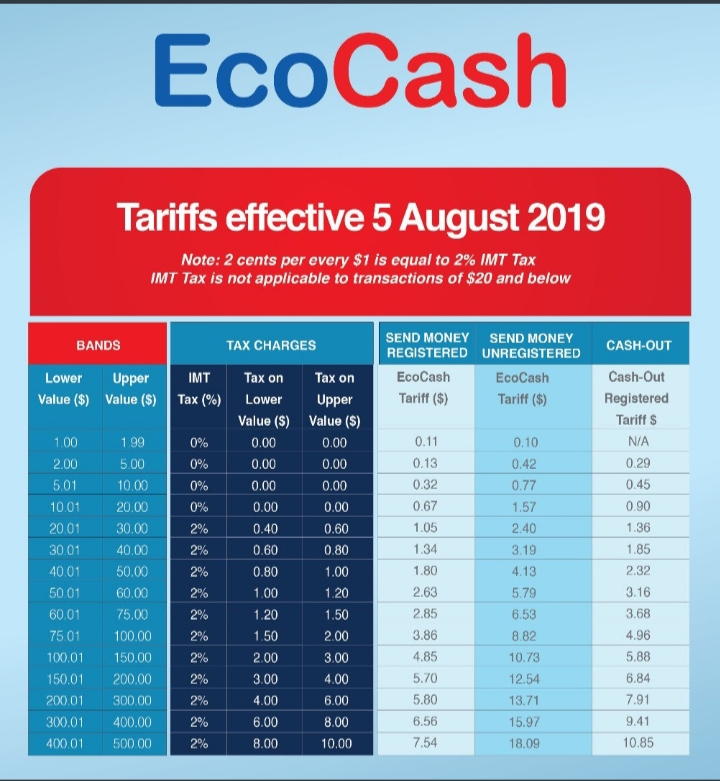

Charges

One of the most important aspects of this debate is charges. Simply put, Zimbabweans care about how much they are being charged to transact.

We recently took a look at charges in the banking sector and here’s a table with those charges:

| Bank | POS fees (transactions below $10) | POS fees (transactions below $20) | POS fees (transactions above $10) | POS fees (transactions above $20) |

|---|---|---|---|---|

| Agribank | $0.20 | $2 | ||

| BancABC | $0.50 | $3 | ||

| CABS | 0.5% (min $0.40 – max $6 ) | 0.5% (min $0.40 – max $6 ) | ||

| CBZ | 2.5% (min $3.00 – Max $25.00) | 2.5% (min $3.00 – Max $25.00) | ||

| EcoBank | 1% of the transaction value | 1% of the transaction value | ||

| FBC | $0.20 | $0.74 | ||

| FirstCapital | $0.30 | $1.00 | ||

| Metbank | * $1.35 min – $5 max (* thresholds not specified) | * $1.35 min – $5 max (* thresholds not specified) | ||

| Nedbank | $0.50 | $2.50 | ||

| NMB | $0.50 | $0.50 | $1.85 | |

| StanBic | $0.20 | 0.5% – minimum $0.50 and maximum $10.00 | 0.5% – minimum $0.50 and maximum $10.00 | |

| Standard Chartered | $0.19 | $0.85 | $0.85 | |

| Steward | $0.80 | $1.65 + 0.05% of transaction value | ||

| ZB | $0.93 | $0.93 | $0.93 | $0.93 |

How do these charges compare to EcoCash? Well, it’s a hard comparison to make for a number of reasons including the fact that it’s a comparison between one mobile money institution vs 14 commercial banks which have different charges.

Another problem with this comparison is that because of the aforementioned reach and distribution of mobile money there are some cases where even if your bank is the cheaper option, it simply might not exist in certain areas which negate the advantage of being cheaper. For instance, the social norm is simply that if you want to perform a P2P transaction to someone in the rural areas you use EcoCash. In such situations it will not matter if banks are cheaper because i) there are no POS machines in many of these areas and ii) there are no ATMs to withdraw making a bank account an afterthought to the people in these areas.

Finally, another aspect that makes comparing charges between the two mediums difficult is the current lay of the land when it comes to charges for withdrawing/cashing out.

Withdrawing money from local banks is one of the best patience building exercises known to man. There’s uncertainty on just how much you’ll withdraw and because of the time it takes to withdraw citizens have all but given up when it comes to withdrawing from the banks.

If you don’t live in Zimbabwe, you would assume that this means cashing out through EcoCash is a clear winner – and whilst there are no queues or uncertainty over amounts you can withdraw, there is a different kind of devil you have to contend with. EcoCash agents understand that money is scarce and have begun selling money to whoever is interested in cashing out. The cash out premium has gone as high as 60% negating the convenience of avoiding bank queues and withdrawal limits.

In terms of charges, none of the two offers a better deal and I would call this a draw…

Swipe 3-4 EcoCash

So what’s actually better?

Well, as with most things, it’s really contextual and depends on what you need from your financial service provider. If the ability to perform P2P transactions, and easily set up an account is important to you EcoCash offers more. But if speed of transacting and fewer downtime issues are more important than that bank card will offer you a better experience.

As most of us will know, a hybrid (or having both) is actually the best setup because both banks and mobile money have pros and cons which make them integral to most of our lives and ditching one exclusively for the other will definitely mean missing out…

Comments

16 responses

Why do business people charge 50% on to of their prices when one pays with ecocash/one money etc?

This is another biased comparison that keeps you guys getting branded as a pro-Econet mouthpiece.

*Ease of Setting Up*

First you MUST have an Econet line, which pulls in its own KYC requirements to get. ONLY after that, may you apply for EcoCash. The “swipe” KYC process, you have outlined, actually relates to opening a bank account. A bank account has no card by default and applying for one is just as easy as applying for EcoCash. It is just that we are accustomed to apply for the card at the same time we are applying to open an account, so you think it is one process.

Swipe 1 – Ecocash 1

*Speed*

Swiping is 2.8 times as fast as EcoCash and you have given them an equal score, honestly? Those speeds were probably on a good day as well. There is a reason some shops relegate EcoCash customers to their own queue. That is because EcoCash transactions can be incredibly slow.

Swipe 3 – EcoCash 1 (In proportion to the speed and since scoring system is a mystery)

*Convenience*

I would argue that you are actually more likely to leave/forget your phone (if you are a guy) compared to forgetting your wallet. Phones are left on chargers/tables/desks all the time, whilst your wallet is almost always in your pocket. You only take out your wallet to pay for stuff, or get a business/identity card, and back in your pocket it goes. You don’t need to charge your swipe card either, so it’s immune to erratic ZESA, neither does it need network. It’s also not a problem to have more than one swipe card, even 5 can fit snuggly in your wallet. I’ve seen people fumbling to change SIM cards, at tills, because “Iyi ndiyo ine EcoCash”. Even if you had chosen the wrong swipe card, it takes only 4 seconds to retrieve another one.

Swipe 1 – EcoCash 1

*Distribution and Reach*

This point shouldn’t even be there given that most agents don’t offer fair cash-outs, neither do most ATMS carry money. But, supposed we keep it there, an ATM can serve a customer faster than any CORRECTLY processed cash-out. That’s why there’s no need to match the numbers. By the purpose of the tools, swipe is not a money transfer platform, the expansive EcoCash agent network was meant to serve money transfers not general transactions. POS machines are also no longer expensive to acquire as well, Kwenga, Kagwenya and the CBZ mini pos are affordable options.

Swipe 1 – EcoCash 1

*Uptime*

When EcoCash is down, everyone on EcoCash is down. The banking system is rarely down in it’s entirety, or more than 2 banks at a time. Usually, changing a swipe POS provider can solving transaction switching problems, but with Ecocash this is no such alternative.

Swipe 2 – EcoCash 1

*Charges*

EcoCash charges have traditionally been higher than bank charges. It is only in this inflationary environment that bank charges have caught up, but I reassure you that on the next EcoCash tariff adjustment things shall return to the norm. Anyway, I will leave that score unchanged, since the comparisons are as at current.

Swipe 2 – EcoCash 2

What’s the point in scoring a comparison and not providing a final tally???

Swipe 10 – 7 EcoCash

KYC – You don’t require an Econet line anymore and you can actually open an EcoCash account with a telecel and NetOne line. Yes the KYC for opening these accounts is a bit more complex but it’s still less complex than what you need to open a bank account.

Speed – Each category was being scored a point each my friend. Swiping had no point and got it’s first point hence 1-1

Convenience – I guess I’m a different type of guy and considering that when people go out they need their phones to actually communicate with people they are meeting etc I would counter argue that it’s easier to forget your wallet.

Distribution and reach -the issue of cash out charges was addressed in the next section that deals specifically with charges.

ATM’s are not faster in Zimbabwe my friend. Not when you consider that you have to wait in line for 2 hours to get to said ATM and initiate the faster process you speak of. If the queue and the ATM process is in isolation to you I don’t really know what to say to you.

POS machines are no longer expensive? Why aren’t vendors using POS machines?? Why are they using EcoCash? Because the set up is much lower in cost and the learning curve for traders is higher when it comes to POS machines

You failed to understand the scoring system which was one point per category, maybe understanding that will put the article in a different light.

The KYC is still required for EcoCash regardless what line one has, therefore it cannot be ignored for your convenience.

An ATM is faster that a cash out. What you are talking about is the issue of cash shortages, coupled with the bank you use. EcoCash agents are also affected by these cash shortages as well, I don’t see how that becomes a swipe issue. Plus, banks don’t charge you premiums to withdraw your money.

Affordable doesn’t mean “not expensive”, I don’t think further clarify is needed there. Some vendors to use POS machines and even hairdressers have the Kwenga device. The cost for a mini POS is higher, but it is not prohibitive as you seem to suggest.

The scoring is not one point per category because there are 2 points on some items.

There are 2 points on some categories because the point from the previous category is carried over. So if it was 1-0 and then engaging EcoCash gets the next category it’s 1-1… Seemed simple but guess it could actually be confusing. Thanks for highlighting that

Aha! I see. I had perceived a per item scoring, my bad…

Lastly, you of all people who reads Techzim everyday suggesting that we are a mouthpiece for Econet is quite disappointing because I would expect that because you’re one of our most loyal readers you’ve seen us objectively call out Econet on multiple occasions. But nope, when it’s convenient we’re an Econet mouthpiece and when we call them out you’re silent.

Didn’t expect this lack of objectivity from a reader who consumers our content on a daily basis.

But most importantly that is your opinion and you’re entitled to it and hopefully you keep engaging with us when you see it fit to do so…

You must note that I merely suggested that articles like this are the cause of folks to brand you as such. If you have read OTHERS comments on your website, it is has been suggested many a time. This article makes me lean towards agreeing with them, that’s all.

Anyway, I am loyal to tech and reading, not necessarily TechZim. I read Technomag, Htxt and Techunzipped with similar frequency. But, I don’t think being your frequent reader is a logical basis for me agreeing or disagreeing with you. Does frequently reading your blog make it more correct?? I’m not sure where the lack of objectivity is presented when I clearly outlined my perceptions, instead of just disagreeing without a point of reference.

These are my opinions, there’s nothing important about it. EVERYONE has an opinion about something, so do not get upset about it. Mine is just very different from yours.

I never said being a frequent reader means you should agree with us. What I said is that being a frequent reader should give you objectivity to know that we’re not an Econet mouthpiece. Pretty simple stuff really.

“Imi Vanhu Musadaro” you write as if you a personal agenda with Techzim. I am surprised you wrote a full article of your own kkkkkk, instead of simply pointing out (in summary) the areas you don’t agree with. After all, ANYONE is free to express their thoughts, Techzim included. It’s not a war, dude, to prove who is smarter. It’s not Math, where 1+1 always equals 2.

I had the time… Though if I was TZ, I’d be asking “Why are you commenting on this comment? You never commented on my other comments”. LOL

I think the charges of ecocash is a real problem…which is where swipe takes precedence…the other thing is online transactions…I for one prefer ecocash than giving out my bank details.security…overides price

I agree with your opinion overall no clear winner and each had it’s uses…

Hey totally missed the online purchases and security aspect, thanks for highlighting that. It’s definitely one category where EcoCash has an advantage because your security details are never being shared on the platform you’re transacting on 🤔

End of the day performance and charges of both eco cash and banks are PATHETIC!

End of the day the performance and charges of both Ecocash and banks are PATHETIC!

On speed and convenience Swipe is at least five good points ahead of ecocash. You don’t have to charge your card, it doesn’t need to have a network connection itself and it doesn’t freeze like a phone does. Merchants who only use a merchant code vs the simple zimswitch online also make ecocash less convenient and slow. Transaction failures can also be way more complicated on ecocash – on swipe you are simply declined and that’s usually the end of it. On ecocash you get issues like the message didn’t come, it left my wallet but it didn’t arrive blah blah. User side errors from ecocash as well, where you input the amount wrong and then the topup is now less than ecocash minimum – or the rare but still present possibility of sending to the wrong merchant code. Most people know to verify first, but that verification is AGAIN taking away from the speed. You guys should consider also attaching polls to some of these things coz you tend to write from your own totally out of touch perspectives and end up rubbing your readers the wrong way