A few days ago I noticed vPayments finally has easy to integrate plugins for e-commerce CMS like Opencart, Magento and OScommerce and I immediately downloaded for an Opencart store I was experimenting with. This is a good development considering that less tech savvy e-commerce startups would otherwise have trouble integrating vPayments using pure code. The new plugins mean that Zimswitch has cleared a major technical hurdle that will hopefully see a lot more businesses integrating vPayments.

However, although the technical hurdles are slowly moving out of the way, the payment platform still has a long way to go in clearing red tape and in becoming more visible.

Once you install the plugin, you still have to do find a vPayments enabled bank to sign up for a vPayments merchant account and the process can be extremely frustrating. Currenlty, you can only obtain a vPayments merchant account through four banks namely ZB Bank, CBZ, CABS and FBC and you will need a business or corporate account with any one of these to be connected.

Opening a bank account in Zimbabwe is frustrating for a lot of people and opening a business bank account is even harder. ZimSwitch should obviously move fast to integrate other banks so that at least people have more options or some can find a bank that they already bank with vPayments ready, from a merchant perspective.

However, major frustration point was that none of these banks’ customer interfacing stuff had a clue on what vPayments is or what it does and I had to ask for “someone who does ZimSwitch” to get pointed in the right direction – or to least get closer to where I wanted to be.

I spoke to one senior executive at one of the vPayments enabled banks and it increasingly became clear that vPayments is down the perking order of priorities as they indicated that their particular bank may not even have a marketing budget for vPayments. Obviously these banks think there is no “real” opportunity with vPayments – at least not on the EcoCash or mobile money scale which they obsess about.

Whilst you would think as a product, vPayments is getting better from a technical view, their awareness strategy leaves a lot to be desired. It seems a lot of that has been left in the hands of banks, who clearly have bigger fish to fry (liquidity, minimum capital requirements targets, etc).,

The fees are not as standard as would be natural since with vPayments, you are dealing on one platform controlled by different banks. For example, some of the vPayments banks have a minimum transaction value that will cost you more if you fail to reach. In this case, FBC and ZB Bank say your vPayments merchant account has to process transactions worth $50 and $75 per month respectively before they can effect percentage based transaction fees which is 2% for both banks. If you fail to reach the transaction value, they will charge you $50 (FBC) or $75 (ZB Bank) for that month. So in essence, simply sell more or pay more.

CBZ and CABS have a flat 1.5% and 1.99% transaction fee rate.

Vpayments merchant transaction fees

| Bank | FBC | ZB Bank | CBZ | CABS |

|---|---|---|---|---|

| Branch | Nelson Mandela | Speke Avenue | Samora Machel | Borrowdale |

| Transaction Fees | 2% | 2% | 1.5% | 1.99% |

| Minimum Monthly Transaction value | $50 | $75 | nill | NILL |

These variations probably re-affirm that with vPayments, much is left to the banks which is a sharp contrast to what Econet did with the highly successful EcoCash. With EcoCash, the owners of the platform were at the forefront of pushing it and making it successful. On the other hand, it seems that the people at ZimSwitch are technical consultants for banks who see little value in the product at this current stage.

The risk vPayments is carrying by not milking this product early on is when (it’s a matter of when) Econet comes with an online payment solution, vPayments may simply die a still birth. EcoCash is a prime example of how Econet is relentless in implementing or rolling out products. NetOne’s original OneWallet and Telecel’s Skwama are well documented case studies that with Econet in the picture, being the pioneer counts for nothing.

We also hear that another company that is already well integrated into our local banking system is set to release another online payments platform. This particular company is world renowned and there is no doubt that they have what it takes to create a payments solution to rival vPayments.

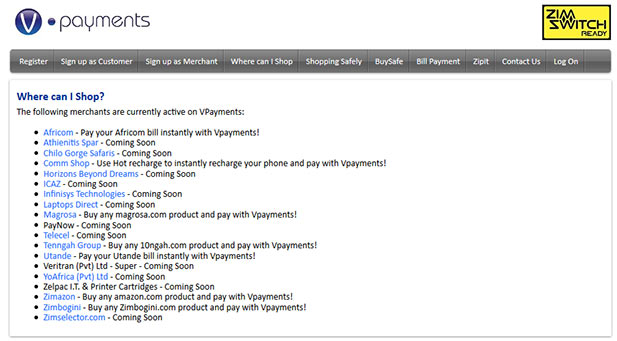

vPayments should definitely do more for awareness in 2014. Right now, only a handful of merchant are listed on the vPayments website suggesting a slow uptake for a relevant and arguably overdue solution. 2014 is the year that vPayments needs to get a stronghold on the market or risk being cut out by new, more aggressive competition.

6 comments

You might need to change your spelling of ‘beaurocratic’ to bureaucratic

Visa?, Mastercard? Visa huh? Full Visa integration is coming to Zim huh? Say yes please!

Hi TechZim Readers

Happy New Year! I think the article above have some important points. eCommerce is new to Zimbabwe and it has been an uphill fight to get the V-payments platform this far. However, I think it is also important to note that the platforms are now in place and most of the bigger banks are certified and live, with the remaining expected complete early 2014… it is now up to the eCommerce merchants to start enabling the payments options! We at ZSS simply do not have the budget to make the kind of “national marketing noise” mentioned above, but our hope is that between the banks, the merchants and the customers we can get it to where it needs to be.

Just a few extra facts to add to the article, specifically around Super-Merchants. This enables merchants to integrate directly with a (non financial institution) super-merchant who has already certified with an acquiring bank. This should make mass scale integration much simpler and convenient – no matter the merchant size. Larger merchants will probably prefer a direct relationship with the acquiring bank, but our hope is that the Super-Merchant functionality will satisfy the smaller merchant’s requirements..

1) While standard V-payments integrations for merchants do require a full merchant account at a V-payments certified acquiring bank, there are also sub-merchant connections available through Super-Merchants. WebDev offers an “off the shelf” solution for this based on OpenCart, while stand alone sites can contact support@zss.co.zw for a direct integration to stand-alone websites through any cart system. More Super-Merchants are expected soon. (membership and transactional charges will vary by super-merchant)

2) Some Super-merchants can also offer full (and completely legal) Zimbabwean initiated and officially settled Visa payments. (This is also available direct with CBZ). Additional “legal” international payment options will be available soon!

Hope this helps – but please feel free to post more questions here on TechZim, or email support@zss.co.zw directly for more comprehensive support.

Thanks for clearing things up Adam!

This is what we have been waiting for, for the Zimbabwean digital economy to explode.

Agreed Greg. Also in vPayment’s defense there aren’t that many eCommerce upstarts in Zimbabwe but they will come slowly over time until we enter our own bubble.