EcoCash has been in the domestic remittance game for a while now. In the service’s over a decade life, competition has never been stiffer. What was once the no-brainer choice is now just one of many options.

The regulators saw to that. As we speak, using EcoCash in the way we used to is not advisable if you’re sending USD. You may have experienced this, the charges are excessive if you cash in, send money and cash out using EcoCash FCA wallets.

Here’s how you’re charged for that:

- Cash in – 4% IMTT

- Send money – 4% IMTT (plus EcoCash’s cut)

- Cash out – another 4% (plus EcoCash’s cut)

Do you see that? You are charged 4% Intermediated Money Transfer Tax at every step. It’s ridiculous that you have to pay to deposit USD into your EcoCash FCA wallet.

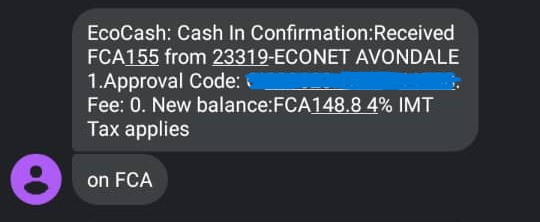

I tested this myself? I deposited $150 into my wallet and this is how it went.

- Cash in $155 and New balance = $148.8 [Tax of $6.20 charged]

- Send money – $141, New Balance = $0.2 [Tax of $5.95 and EcoCash fee of $1.65 charged]

- Cash out – $137 [Tax/Cash out fee of $3.04] which is not quite 4%

Screenshot showing the 4% IMTT collected on a cash in transaction.

Kind of tax is this?

This kind of taxing is meant to stop you using the service. How can each step in the transaction process be treated as a stand alone transaction?

EcoCash consulted with the regulators and it was revealed that this is how they are supposed to charge the 4% tax on EcoCash transactions. You are probably thinking, ‘how come no one else is charging the 4% this way?’ That’s the million dollar question.

We reached out to OneMoney to find out how they are doing it thinking maybe it only applied to mobile money operators. That’s not how they are doing it. They only charge the 4% when one sends money. There is no 4% tax when cashing in or cashing out.

I didn’t test this myself but that’s what they say.

So for some reason , only EcoCash is charging the 4% tax the excessive way. Off the bat, we can rule out EcoCash collecting these charges for themselves and lying that they are taxes. There really is no upside to them doing this.

EcoCash would not intentionally make their service the most expensive. They are losing market share because of this. Besides, the regulators keep an eagle eye on EcoCash transactions and there is no way they could get away with it.

So, the question remains, ‘why only EcoCash?’

The smart way to use EcoCash – the voucher

The charges above are atrocious. My recipient only received 88% of the $155 I deposited. So, taxes plus EcoCash charges reached an ungodly 12%. Let’s come right out and say it, until something changes DO NOT cash in USD into an EcoCash wallet.

There is a way to still use EcoCash that doesn’t result in 12% charges though. If you use EcoCash vouchers you won’t be charged the 4% IMTT multiple times. It becomes a straightforward affair.

The Voucher works like those other remittance products.

You just walk into an Econet shop, provide the cashier with your ID, the money to be sent and the recipient’s name. A voucher number is generated and sent to the recipient. The recipient uses the voucher number to collect the funds.

The charges? There is no cash in or cash out charge. EcoCash charges 3% and the government gets its 4% for a total of 7%.

This compares favourably to the other remittance services in the market. We looked at how InnBucks is coming in hot, charging only 1% to transfer and 2% to cash out.

Sending $150 using EcoCash vouchers works out to $10.50 in charges. Using InnBucks the charges reach $10.35. The 15 cent difference is not significant enough to choose one over the other. It will come down to which service has a shop/outlet near you.

The collection point

InnBucks comes in boasting over 260 locations across the country.

EcoCash used to have merchants in the thousands but that was a while ago. When it comes to vouchers, you can only transact from Econet shops and there are fewer of those than there are merchants. They should be in the hundreds though. We will update this with the actual figure when we get it.

I tried using the EcoCash vouchers once and the shop at my recipient’s location said they could not release cash if we used the voucher method. They instead advised us to use the expensive cash in/cash out method. We reached out to EcoCash on what that was all about and they are looking into it.

I have heard some complain that the collection process can be slow at InnBucks locations because one has to queue up with those looking to grab food at the Simbisa outlets InnBucks uses.

Anyway, that’s just a quick comparison between EcoCash and InnBucks. We shall compare all the domestic remittance solutions in the market. That should be fun.

Also read:

InnBucks is back as a bank, is it still as low cost as it was before?

14 comments

Is it possible to receive money in innbucks from the UK?

I don’t think you can yet.

I don’t think you are supposed to be charged IMTT when cashing in, because the funds still belong to you. That is, you are the source and destination. Are you sure it isn’t the banks fee?

That’s the crazy bit. Didn’t understand it either. Talked to EcoCash and they confirmed that indeed they were instructed to collect IMTT on cash ins. I have updated the article with a screenshot of the transaction. It is mad what the RBZ is doing.

Wow. It’s a sad state of affairs.

It’s indeed a sad state of affairs,I mean how can you be charged for cash in ??????

Regulatory issues yes but then I don’t entirely trust Econet and its babies like Ecocash. On this one, if true, it’s fairly obvious why regulators would want to limit Ecocash operations that way. Let me go off topic a bit; without any regulatory eye on their transactions, what stops Ecocash guys from “creating” money within their systems and increasing money supply in the economy while concurrently harvesting USD from the public??

Nah Ecocash can’t just create money, if I can do that that means we have a useless government which can’t account for all money in this country.It would mean that banks are also doing the same with the RTGS system.The main problem here is the ministry of Finance they should be aware that they are double dipping through their tax system, they are essentially taxing everyone twice and if you have noticed even some bank charges have increased as a result of these ‘small’ taxes.

Regulations don’t stop fraud, audits and oversight do. ZIPIT could equally “manufacture” cash. Technically, any bank can inject cash into RTGS, ZIPIT or Ecocash platforms from a non-existent source account. Anyway, the truth is, we all know where the excess liquidity comes from, but instead some choose to bury their heads in the sand.

Regulators creating unfair competition to downthwart ecocash.

Nah Ecocash can’t just create money, if I can do that that means we have a useless government which can’t account for all money in this country.It would mean that banks are also doing the same with the RTGS system.The main problem here is the ministry of Finance they should be aware that they are double dipping through their tax system, they are essentially taxing everyone twice and if you have noticed even some bank charges have increased as a result of these ‘small’ taxes.

Inga ma 1 aya Ecocash yacho yakubatira vanhu iyi. Tongoti Econet yese hamheno zvairi these days, Netwrk yacho kutenga bundle ropera usati warishandisa zvakakwana.Ecocash ku linker nema bank chaiko ma 1,kubank inonzi account yaka linker ne Ecocash but ukada kuita access ma banking services pa Ecocash unonzwa kuti “Account does not Exists” hamheno chirudzii ku bank zvichinzi zvaka linker. The whole Econet System is weak now nekuda kwekungo upgrader non stop vachichinja ma prices ema bundles avo.

The most naive assumption would be to think that the problem lies with EcoCash.

From understanding here, EcoCash not the problem, but govt taxes, being charged to put my money in my pocket