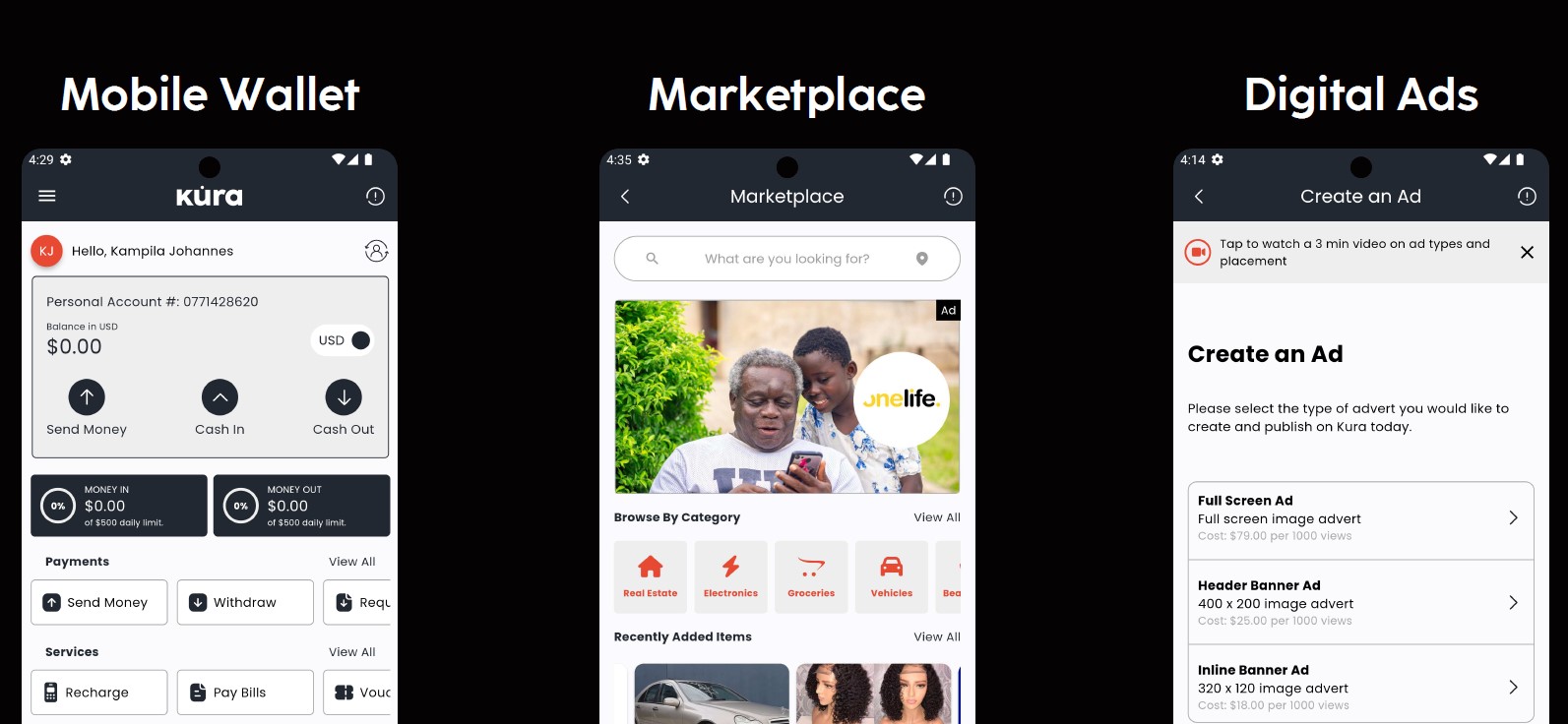

A Zimbabwean tech startup, Kura is hoping to upend the mobile money market with a digital wallet that offers consumers no fees for transacting. The service, co-founder Michael Charangwa explains, achieves this through a set of services that includes ads, a marketplace, and other things that collect and leverage customer data.

Charangwa says the digital wallet, which is called KuraCash, is set to launch in June this year if there are no major hiccups on the regulatory side of things.

Kura is positioning the wallet to compete against dominant wallets in the market; EcoCash, Innbucks, and to an extent emerging ones like Omari that are also trying for a piece of the local mobile money, money.

The main idea, according to Charangwa is that while mobile money has been a big success across Africa, the fees charged to customers are quite high, negating the benefits of this innovation to consumers. And considering the amount of back and forth transactions between people and and when they pay small businesses (Msika, kombis, tuckshops and more) the cumulative fees charged on the same dollar circulating several times a day can be astronomical.

So the ads will pay the fees. But anyone that it’s in the digital ads locally knows the yield for ads in Zimbabwe is quite low. How much ad viewing and clicking would it take to pay a few transaction for, for, say, $10?

Charangwa explains that brands are not willing pay much for ads currently because the targeting is too weak.

“The underlying problem [with the low cost per click] is the unavailability of data. If someone in Zimbabwe were to click an ad, there are currently very few points the person can be identified by. And this is a big African problem. If an African consumer and an American consumer both have $10, I get more insight on the American than an African, and it’s really a data insight issue.”

So given all the data KuraCash will gather, thanks to KYC, they have, in theory at least because the app hasn’t been released yet, the startup will have better and better targeting. Better than or even good enough to get relevant ads from advertising platforms looking to target Zimbabweans. Kura itself also plans to build out its own advertising platform selling inventory to local brands directly.

Charangwa says the marketplace will just add to this rich data they’ll have on everyone using the platform, leading to even better targeting, leading to better performing ads, leading to more ad revenue, which would allow them to offset fees they’d have needed to charge for the wallet services.

And when this flywheel works well enough, it might even get to the point where they share some of the revenue with users of the app – rewards – for things they do within the app.

Chicken and Egg

So how will KuraCash get enough people using the free mobile money so that it’s attractive to the advertisers? They’ll need to invest in an extensive distribution network (agents and merchants), awareness, so customers feel its visible and liquid enough to try.

That certainly looks like a huge cash outlay, time investment and just organisation building, to get it all working – especially if the objective is to challenge the big boys in the game – and to do that with a no-fees strategy. It’s literally spending lots of money for nothing in return, for a while.

Additionally, marketplace sellers will also likely see no value in listing their products unless there are lots of people transferring money.

Charangwa says they are no under illusion that there will be a period of spending on the network and the costs of transacting until there’s a critical mass attractive enough for advertisers to spend on. In fact he says this is no bootstrapped startup. They are raising money specifically for this purpose, targeting investors that are happy to put money until everything is in lockstep.

How long a runway they will need until the components of sides of the business model are feeding each other seems clear enough to the founders – several months at least he says.

And what about the taxes?

One complication of providing a zero-fee wallet is the taxes. The tax-collector is incentivised to collect, whether the provider has charged a fee or not. Charangwa admits this cost cannot be innovated away.

If Kura manages to get customers using their wallet, customers will be incentivised to send big amounts using the platform, which means government will just want even more tax. Charangwa assured me in our conversation that the model will still hold.

The Cost of Mobile Money

Charangwa also says they are going to be quite aggressive keeping the costs of the service down. He says mobile money providers incur significant costs at the point of cashing out, so Kura’s strategy is to give customer no reason to cash out.

Competing against incumbents charging an arm and a leg, and a government wanting its tax is one thing – a hard thing, just to be clear – but can KuraCash win against Cash.

Charangwa explains that people only use cash because mobile money providers’ fees are too high. He also argues that these incumbents don’t have a wide enough merchant network to guarantee customers they can spend anywhere with the wallet.

There are definitely challenges – taxes not least of them – of providing this alternative take to digital wallets. If KuraCash can successfully navigate them, it could reshape how Zimbabweans use mobile money, and maybe even Africa. Time will tell.

51 comments

All these money transaction startups are after the green💵💰.To be honest I’ve been thinking of starting mine too called Tumira Mari Wangu (TMG💸💸💸)🙃🙃🙃

I wonder how one will even think of dethroning Econet when they are primarily using an Econet line for their USSDs(*569# Innbucks). And others like Paynow just use EcoCash adding more income on the Econet part.

Our idea after the deal with Africom was to add as many value added services as possible and have data at break even. Izimali was going to be a Mastercard/Visa with loyalty points and all sorts of Carrots. For that we needed a BIN number from a local bank. We spoke to one of the biggest foreign banks, but I do not think they understood what I was there for. Water under the bridge. The incumbents do not realise that the industry can become more innovative even if the startup owner does not arrive in a Benz. You all came from humble beginnings but when you are now on that side of the desk with a suit and tie, you look down upon a jean and shirt wearing tech startup owner who can generate billions in revenue, but you can not look past that. Must be lentils,those things make people think they are super human. You are losing to Kenya and South Africa, well the World in General but you gloat, it’s strange. If you cannot identify and nurture talent,you should nowhere near a job that requires human resource management, or an manager role for that matter. People matter, therefore customers matter. So instead of saying why is your Data offer so generous, ask how we will make money and I will show you. We need a corporate governance policy like the King Report in South Africa. Their companies are kicking our companies asses, that’s why your import bill and your brain drain is so high. Yes, I was in the Vodacom board room, yes I went to represent Altech ISIS in the Standard Bank Audit. They have a different way of running things, it’s not perfect but we can learn a thing or two. Like giving Employees laptops and data, car plans, housing plans, school plans. Not just for the suit wearing men in black,but for a reasonable standard of education, without and within the organisation, and work ethic. Don’t even get me started about venture funding. Internation VCs are looking for charity causes, local VCs are looking at stealing ideas, so need to change this culture because we are shooting ourselves in the foot. The Fin Min, before he held office and it’s trappings, said he would create a Venture fund. The idea was good but……We wish this startup the best of luck, and pray they succeed and succeed well because we need all the tax revenue we can get because we are going to lower and remove some barriers to production. #DataMustFall

I’m sure you make some good points but your writing is so garbled its difficult to understand

I know. It’s had to comprehend. It’s okay, you can use Google translate into most other comprehensible languages. How is work today? Is everyone at their desk or they went for lunch?

This brings to light the predatory transaction tax. In-house transfers should not be taxed, ie, if you are an ecocash user sending to another ecocash user such transactions should not be taxed, because the equivalent transaction done using cash would not attract any tax charge, it should be the same for electronic transfers. That would put cash and e-money on equal footing. Only transfers coming into and out of ecocash to and from another service should attract a fair tax. Also retail transactions should be exempt from transaction tax charges, because again the same logic applied to in-house transfers applies here as well, and on top of that, there is the VAT charge.

Besides where is all this money going. Its certainly not going to civil servants, nor is it being used to improve service delivery. NXA!!!!

The taxation system as a whole is predatory

Yes tax should be fair not squewed in one direction unless you are building a rocket or something tangible to sacrifice for, not imported cars, serious madness. Some of you we would like to read your school reports and what your teachers said about you. Did you play sport, did you participate in clubs and societies. Where did you go to school man, where did you come from?

Mthuli was ordered to milk the GOAT (grown ordinary adults taxes) so aint no coming back from our skinny hides. Ah look we now have sugar tax… And it’s not for the diabetics

Is that really viable? Looking at this wondering if they are being too naive and hopeful. Better way would be to just offer a low cost service and zero rate it later

Only if the value for transacting with could be stored in air and the sun could be used to move the value during transactions, can they provide a service that is free to the user.

It was once said the population application which even go is now using was supposed to be free, and the owners of the transport means turned it into a cash cow which no longer grazes on local stuff but the international green matter!

With companies shrinking and advertising being a cost they usually do away with, it will really be a miracle for the service to be run. Well, someone sang “The chances of anything coming from Mars are a million to one, but still they come”, lest I sound like a prophet of doom.

…… which even gogo is now using was supposed to be free, and…….

If Vodacom or MTN where to launch in Zimbabwe, would people move to their Network? Brand loyalty may just be loyalty to a current better option, people are will to play higher to better service. Like 99 Octane for BMW Drivers. If the option is only E20 then what else can you do. Oh, I met a lady from Vodacom in Zambia at the NGTELECOMS summit in Sandton. They had an interesting concept, data centric,haven’t been in touch,but Chirundu panofambika. They are beating us, we have to wake up, we have no time for games, or else will be like those countries in Africa that you used to laugh at. #DataMustFall this Fall.

Exactly! We stick with the likes of our service providers because we have no other choice and there is no real competition. Let Vodacom. Musk et al come in and then see

Yesaya. Competition brings out the best in us. That Liverpool Mancity game was insane, that’s why we watch the Premier League even though we have to stump out forex for subscription. Good we’ll run football that’s all, and people come.

We have so many mobile startups that have promised to reshape how transactions but they forget there is what is known brand loyalty.

Some people would not move away from Ecocash even if the way of doing business with it is very high.

So I have always had this idea of opening a Bar. Hint it won’t be at Unit J Shops, we already have enough Bars, maybe we could use a coffee shop or bakery. The Bar will be called Gen. Tekeshe Bar aka Delta Charlie 13. It will have all sorts of art, Shona sculutres from up the road, a fish tank (yeah! because I had to release my beloved fish into the Liesbeek Canal because they next day I was flying back to Zimbabwe, this is late 2014. Oh yes our Bar will have FREE internet after you buy something anything, even Mudzanga weRemington Gold, BOSS,Chief or a token to play Street Fighter Zero Two, but do not come in flip flops or the lads and lasses will show you out. Ah man our DJs will be well paid,and we are currently looking for a local company that can make speakers sound like Bose, and others to make a Dobly like platform, maybe these local features could make their way into the Lizard X1, like Beats Audio on HP. Asi Super and Nyathi bho, unlike some VIP Bars…kkkkk God willing you can come do your KuraCash transactions there, while we serenade you, or and there is Pizza $1 a slice. Hint the Bar will be in Mozambique. #DataMustFall

Morning lads and lasses, does the ICT Min. Read these posts. Actually,when he reads, does he comprehend them. My constant fear is men in suits doing IT stuff. When we went with investors to meet his Predecessor and PM. We left there thinking boy, that stuff was going over their heads, or not they just didn’t this kid from a compound, kunge Ivo vakabva kuChishawasha Hills, Silver Spoon gated community. We once hosted one of the founders of Vadacom SA. Mr. Allan Beets with Bert Dogart in tow. With my team at the Meikles, and we drank some expensive coffee for it was a happy day. Then they saw kuti mupfana uyo. Vharai vharai, achatinetsa…kkkk Ndichirikushereketa, ndorova Sub baba, ndorova Sub. Izvi Zvikomborero baba, Zvikomborero. The Revolution songs are now against you; the land, the wind, the water, the plants, the animals, the people, the Lord has rejected you! Woe to your generations and future generations may they live their entire lives compensating for your bull$hit. Begone! Demons, Zvikwambo, Varoyi and your Earthly God Lucifer!

Personally I think its a good thing that there is very little data on African consumers given the uses to which such data can be put. Even in countries where data protection laws are the best in the workd there s still abuse of personal data

Kkkkkk I like your sarcasm.

With an EXTREMELY tough operating environment, predatory monetary authorities and the like, there is very little room for companies to advertise. Those that do are going to want to use the small advertising revenue with the places that are known to have the best advantage

Sounds very optimistic but the environment is hostile. They might be underestimating the capacity of regulators to interfere. Also competitors will not take this lying down. The Zim market isn’t that big and becoming ubiquitous will take months to years of burning through precious USD. I also don’t really see a USP besides the ‘free’ charges. Instead of building a new app there might be merit in integrating their payment solution into whatsapp and Facebook. Leveraging existing networks and scaling the ad business as opposed to to reinventing the wheel. All the best though to these brave pioneers.

Payment systems in Africa are quite expensive and difficult to maintain. Human Centred Design will lean on the target customer’s needs. The African market is very sensitive with lags in transfers, cashing out, transfer limits etc. This can be a success only if extensive research on the target market is conducted thoroughly.

Colonial hangover. Perhaps the Freetrade area will solve these legacy issues. Our economies were created to send precious items to other realms. Even heads of our Mhondoro,writing,science,art or manner of items, can we now say Gold without fear. They took it by the ton load, to their credit they used it wisely, have you seen their economies, or just buildings, schools, roads even their movies are good.

Then comes a country that calls their citizens poor as a slur. Kuva nenyota makumbo arimvura.

KuraCash please may I be your first advertiser. After this fall, people can watch the trailer on your platform.

Here are part 2 of my notes on my current work in progress AD 2060. The book will be more comprehensive than the movie or series. There is a bit of a spin off from the African Dance Movie, with a few change of character names, but Ft. Lt. Sibongile remains the same.

AD 2060 Notes +2

Wing Commander Sibo, loves the purple sunsets on Mars and each evening takes her boy to see them. After the death of her boyfriend, she never remarried. Her son wants to join the Space Commando’s but remembering the death of the father of her child while pregnant in a robbery* she cannot stomach it, but eventually consents.

Evidence of life is found by Scientists in Seven Sisters cave. The news is heavily suppressed on Earth until it is leaked to the general public, renewing interest in the Mars Colony again.

A plan for Mars tourism, after the first war to bring the planets together, and an annual sports tournament is planned. Leading to the infiltration of Mars, and it’s almost destruction by a terrorist attack. 2/3 of the Martian population is killed, plus life support systems, farms, research labs. The mines are untouched. Earth claims dominion over Mars and resources and technology are extracted and brought back to Earth ending the Mars golden age of great houses. Martians escape to the Underground caverns and live their simple hermit like lives. The Knights Order is created, using remaining resources, a number of Martians escape to Titan and start to rebuild their colony. Contact is made with a civilisation on Alpha Centari that monitored the Nuclear blasts on Mars and Subsequent nuclear winter. The former Martians now Titans have a powerful ally, and are determined to help the Titans retake Mars for the sake of humanity as the Alpha Centaris are Homo Sapiens Sapiens as well and share 100% DNA with modern Africans.

Dziva in her engineering of the human species strated another civilisation on Alpha Centari after Lucifer tinkered with the human genome. A Galactic Alliance is formed between the Aplha’s and the Titans. The Knights Order is incorporated into the Aplha’s society. The Alpha’s are legendary in the making or armour that can stop almost all projectiles and they have developed a hyperdrive.

Earth Surrenders in the third interplanetary war after Aplha Centari Ships arrive at the Moon through hypergates and destroy all or Earth’s Defences in the day of long knives. Not a single person makes it out alive of the Moon Colony and all military and civilian infrastructure is destroyed. Pods drop Alpha Warriors to the surface of the Moon for a mop up, leading to the capitulation of the Earth and the New World Order. The Alpha Centari Emporer gains Earth, Mars, Europa and Titan. Other civilisations take notice of the solar system….—-} Leading to the sequel After AD2060.

Surviving the Avalanche. While on a date Sibo, and Fleet Commander Eric Knight from the Commandos survive an Avalanche on Mars. Triggered by build up of carbon dioxide. They do not radio this in for obvious reasons. Knight is a former Navy Seal of African American origin. The influence major influence of her son trying to join the Mars Defence Force , Commandos. He becomes the father figure in his life.

#DataMustFall #ThisFall

Oh man. I had a agree flight today, then stuck the brick onto the asphalt. Imagine a World where Nhengure would meet Maverick in a bar and exchange pleasantries, but Nhengure cannot stay he has been messing with the Base Commanders daughter and has to flee through the window, over the durawalls andto the 1000cc BMW motorcycle. The movie will be called Top Gun: Jungle Dustbin or just Jungle Dustbin, if Mr.Cruise who has the first right of refusal to play Maverick for one last hoorah. Or we can use a deep fake or a look alike. Just a brunette with a white t-shirt, cowboy boots and a jacket;) No aircraft carriers, just men in short shorts at the Ecology Corps,they spray plants and once in a while have a team furball in their Mig 29s and BAE Hawks. Dust road landing strips, the Congo River, the tropical rain forest, Zimbabwean cultural and heritage sites. Dogfight. BAE Hawk vs Mig 29 Fulcrum, Guns only, Cobra manuva allowed. Camaraderie, cheerfulness in the face of adversity.

#TopGunMaverick #TopGunJungle Dustbin #JungleDustBin #

Run away with your money

Thank you for the article, tambotandara. Please keep them coming.

#FoxTailedDrongo not to be confused with Khalisee’s late husband.

#ASongofFireAndIce

#FatherofDragons

#WatchPartyBegins

I’m convinced that @HE has bipolar

please seek help

before you lose everything

there’s nothing like a free lunch let alone in Zim

the days this company wants to sell to target a small economy like this makes no sense. we are life a province in Kenya or SA

we need to focus on SADc instead to bump up numbers

I really do not know what Bipolar means, something about two personalities I presume. Perhaps a fitting description would be decapolar+. I can assume any personality you want me to be provided there is a base subject to learn from. I can Marcus Aurelius, Mr. Magica, Sherlock Holmes, Sikander Khan or the original badmun Tshaka from Zululand or even Shensea…. take your pick.🤙🏾🇿🇼🇲🇿🇲🇼💕🗡️

#DzidzaikuDzidza

#Sharigan

#CopyNinja

All the best guys. All i can is focus on a niche. Don’t think about going tall to tall with ana Ecocash. Focus on problems in the market like Change or online payments API or something unique.

Also to be successful in this space it’s all about your distribution network. CICO, cash in cash out!!!

is H.E the founder/co-founder of this startup. I have a feeling he has something to do with this. Either way, his stories sound like a fairy tale story, you met with Vodacom President in Zimbabwe? At Meikles😂? And vakaona intelligence yako? You sound like mentally deranged pan Africanist. You center on the greatness of Africans, without realising that you can change the current situation a person is in i.e colonialism, but you can’t change their mentality

Yes my life has been a fairey take. From the farm compound to getting an MVNO Agreement with Africom and hosting one of the Vodacom founders at Meikles. Go on CCTV watch di Dem flim’ or check the passenger manifests.

The fairey take continues until Uhuru.

#Blessed

Every other week Techzim posts startups, 9/10 times remittance startups. Please, dear startup founders, focus on another thing/business. Brand loyalty is real in Zimbabwe, take for example, Mazoe 2L is costing $4.50-$5.00, but I kid you not people are still buying. I was kumusha recently and people rather buy Mazoe, a trusted and loved brand, than other drinks. My point being majority of people including me would rather brace up and take Ecocash’s exorbitant fees rather than switch services. O’Mari is trying but to be honest, most people only got an account just to test and forgot it even exists. Ecocash has been in the game for more than a decade, and still leads. Services have come and gone and left Ecocash there. Take notes, the money for startup yamuchadhandisa try something better like hameno, importing things with fewer taxes. Just create an app let a person view ads, as your proposed framework, and let them have points that can be used to lower their importation bill.

HE. is just blabbering nonsense, this startup will die like most of its companions. Ecocash is undefeated, kwese kwese. Ukaenda kumusha, ecocash, ukaenda mutown, ecocash. Hapana. you cant change 11 years of brand loyalty with one startup. I’m sorry, but I’m being realistic af

LSM kabweza wats going on at techzim seems muri pa strike lol

It will take me a big effort to convince me to stay at State House. I don’t want to stay in Harare I want to stay at Pavlova, near Chenyika, I will work daily on one of our Ecology Corps farms, because a General must be found with his men.

Ok want ot stay in a thatched home, modest but with all the ammenities, all we need is high speed internet.

You can turn State House into a Museum or grant the grounds for a School and or Hospital. I want to stay in the bush. I will hunt with my Dogs. Drive tractors, monitor production, monitor our horses and livestock. Perhaps fly with the lads and lasses on spray mission for our crops. Visit the Medical Center were we train our medics that DON’T need MATHS, just be able to open and close people under fire, with a worthy exit .We will have a Bar, with lots of pool tables, the best meals, because we are farmers, we can feed ourselves, we don’t need to get foreigners to farm for us, then gloat we are good farmers, skiri rakdhakwa. We will have cross bows, night vision, new helmets with tactical support. Our engineers will design all sorts of cool stuff for us, and we will export our produce to make and buy more cool stuff. Yes LAN Parties in the Email Bar, free highspeed internet. XBox, PS, PC games. A snake pit, extraction of snake venom for our use. Drone hunting Eagles. We will have fun defending this land. And we will be equal and respectful.

Our farms will all be connected, and we will have weather sensors, drones, Sniper Scouts, Royal Commando, Kingsguard, Special Forces (Eco1, Eco2…) Marines because we have a lake near by to practice amphibous assault and defence, Cyber, an Airwing…..lots more, an Ecosystem, man it’s going to be challenging work but it will come out SO SWEET. Think about how much revenue 10,000Ha Tobacco, Citrus, Vineyards, Blueberries, Macadamia, Avocado will do for the economy and our bonuses. The first bonuses will be paid in Mid December and the last one Mid January. Yeah because we would have worked hard.

Ndipaseni Gwai.

#Puma

Any connection with Kurakasha or varakashi?

Is this page defunct?Since Leonard Sengere left it is showing some kind of sickness.Its future appears not good if it can produce one article per week.

The new guy seems to struggle with content.It makes me feel left behind.

Would you please Google & paste arti les likewise before we start attacking you & your long initials 😀😀!

But you guys , these guys dedicate their time writing articles for you to read for free, some of you hamusatii matombo tengawo airtime using techzim platform how do you expect them to operate asii. As much as we need fresh article let’s also promote them by any means possible.

100%

They are making money from ads. Plus their site is zero rated on Econet. Easy 💰.

Nice to see you’re writing Limbikani. It’s been a while. Thank you for Techzim.

Thank you. 🙏🏾

Mr is techzim broke ; closing :::wats going on. Dont you have any new articles to write about

Techzim chingotiudzai kuti website renyu rakuda kuti tibhadhare data kuti tiverenge news pane kuita vhiki pasina nhau. Asi Edwin Chabuka ndiye ega chaive chibaba chekunyora nhau

Ko mzukuru ichi nayi? Complain , complain chete? Siyana ne Techzim.

Pfeee.

This will not hold

Not in this country

Give it time, all you need is belief, I hope it will work out