This story was originally posted on Rolling Alpha: Finance and Economics blog (reshared with permission)

Here are words that I didn’t think I’d be writing: the Zimbabwe hyperinflation is re-emerging. We haven’t had any official inflation figures to back that up. But you don’t really need those to see what’s happening.

To be clear: Zimbabwe is not running out of money. There is plenty of it, housed up in the banks and in the mobile money markets. But it’s money that no one wants to use.

How did we get here? Was it the bond notes?

There are plenty of people who like the “The Reserve Bank introduced bond notes – we warned you this would happen” soundbite. Unfortunately, that doesn’t quite seem to tie back to reality. Because in Zimbabwe’s multi-tiered market for cash, the bond note trades at a premium to the “RTGS”* money sitting in the banks.

*RTGS stands for “Real Time Gross Settlement”, which is the domestic payment clearing mechanism. It’s not important to know that – it’s just become the widespread acronym to describe the electronic money in bank accounts.

Just reflect on that for a moment. Here is this unwanted paper currency – one that attracted protests and widespread rejection – and it’s worth more than the money that people have in their bank accounts.

The bond notes also distract from the key fact here: that the most dramatic inflation has come through RTGS bank money. It’s happened insidiously and quietly. And bond notes were a reflection of this inflation, rather than its cause.

So how did we really get here?

Some background for the non-Zimbabweans:

- Zimbabwe uses the US dollar.

- “used to use”

- It was adopted by the Zimbabwean government under the multicurrency basket regime that took over from the Zimbabwean dollar in 2009, when hyperinflation had finally driven the local currency into a near-bottomless grave.

- However, from then on, economic fundamentals meant that Zimbabwe was slowly but surely running out of US dollars.

- And then it began to haemorrhage them.

The basic economic problems:

- Zimbabwe’s government spends more money than it can collect. And it finances the difference by (essentially) forcing local banks to buy treasury bonds from them.

- But Zimbabwe uses the US dollar, which means that the banks are being forced to lend US dollars to the Zimbabwean government. And because we’re now talking about foreign currency, this means that we have to look at the Balance of Payments (BoP).

- Unfortunately on the BoP front, Zimbabwe spends more on imports than it receives in exports receipts.

- Until a few years ago, the ‘extra’ needed was being topped up by remittances from the diaspora, as well as inward foreign loans.

- But then a few things happened all at once:

-

- The commodity cycle turned (so Zimbabwe was earning less money for its mining exports);

- Commodity-dependent export services suffered a business slow-down;

- The currencies of Zimbabwe’s sub-saharan neighbours weakened (so local Zimbabwean manufacturing companies because less competitive);

- So while the diaspora in those countries might have been sending the same amount of locally-denominated money home to their families in Zimbabwe, it became significantly less in US dollar terms;

- A drought meant that any agricultural exports were lower than expected (and the need for food imports was higher than expected).

- The RBZ and the Minister of Finance paid back the arrears on some historic IMF loans (and a few other long-outstanding loans).

- Some erratic government policies meant that foreign loans dried up.

- So the Zimbabwean balance of payments began to collapse.

- And that collapse turned out to be catastrophic when it became clear that civil servants were being paid in export proceeds.

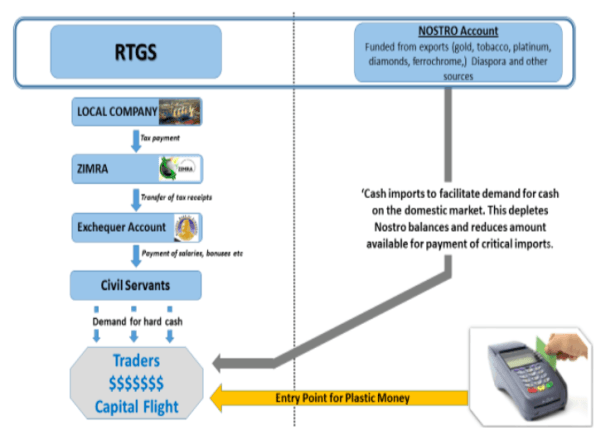

The government tax on cash balances

Here is a bad Balance of Payments situation:

Export Proceeds + Foreign Loans + Remittances < Import Payments

Here is the apocalyptic version:

Export Proceeds + Foreign Loans + Remittances < Import Payments + PUBLIC SECTOR WAGES

To be clear – this is not my own explanation of the problem. This is the Reserve Bank governor’s explanation of the problem – in his September 2016 mid-term monetary policy review.

Here’s the image that was helpfully included in the presentation:

An International Banking Sidebar (consider this some important background information)

Some terminology:

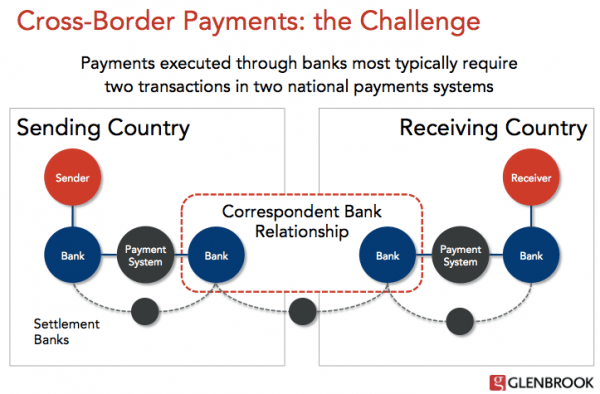

Nostro Accounts: are the foreign bank accounts held by a local bank at a foreign bank (called the ‘correspondent bank’).

RTGS Accounts: are the local accounts within a country (or, at least, that’s what the Zimbabwean banking system calls them).

Here’s a picture that may help:

Basically, the idea is that a US dollar payment from South Africa (Sending Country) to Zimbabwe (Receiving Country) is not simply a US dollar payment from South Africa to Zimbabwe.

Instead, the South African bank asks its correspondent bank in New York to move money to the Zimbabwean bank’s account at its own correspondent bank in New York. When the Zimbabwean bank hears that its correspondent bank in New York has received the payment, it then credits the account of the recipient*. Or, more simply, the foreign payment involves the South African bank transferring money from its nostro account to the Zimbabwean bank’s nostro account. And it just so happens that both of those nostro accounts are held by correspondent banks in New York.

*I know, right? No wonder foreign bank transfers take so long.

The important summary:

Nostro Accounts: hold money which can be spent anywhere in the world.

RTGS Accounts: hold money which can only be spent in Zimbabwe.

This might sound scary, but all it really means is that your local payments get swapped between local banks, and your foreign payments get swapped between the nostro (foreign) accounts of local banks.

And in an economy where the local bank accounts are denominated in foreign currency, there should be a 1:1 ratio between local money and nostro money. Possibly with some variation for local credit extended by the banks to the private sector.

However (the Zimbabwe Hyperinflation Prologue)

In Zimbabwe’s case, there was a really high demand for physical cash notes. Zimbabweans have been burned by hyperinflation before – they want their money to be real.

So in order to meet that demand, the Reserve Bank of Zimbabwe (the RBZ) was regularly cashing its nostro account at the New York Federal Reserve in order to import nice clean USD bank notes back to Zimbabwe.

Unfortunately, cashing out nostro accounts in order to pay civil servants in ‘real’ currency (especially given that almost the entire tax revenue collection is spent on civil servant salaries)… Well now you’re effectively spending export proceeds on the public sector wage bill.

To reiterate: the country was collecting local RTGS payments from taxpayers, and converting those into real-cash-nostro-account balances for civil servants.

This is especially not great when your importers are already consuming more of the nostro account balances than the exporters can replenish:

So when all those issues I mentioned up top started to happen:

- the RBZ inevitably began to run out of money in its own nostro account.

- It then imposed new rules on the local Zimbabwean banks to deposit even more of their nostro balances into the RBZ’s nostro account, in exchange for local RTGS balances in Zimbabwe.

- Those too were cashed in.

- Then when local importers came to pay for their imports, the local banks had no money in their nostro accounts, and had to go request some from the RBZ.

- And then the payment processes started to be delayed until exporters paid money into Zimbabwe – at which point, the RBZ nostro balances would have new money in them, and the local banks could then process the importer payments (if they were high enough up the priority list).

The introduction of Bond Notes

As the RBZ borrowed nostro money against future exporter proceeds, the RBZ desperately wanted to stop depleting those nostro balances in exchange for cash notes – cash notes which then leave the formal banking system permanently because everyone was worried that it might not be there tomorrow.

So the RBZ introduced bond notes, apparently backed by a foreign credit facility, in order to create a medium of exchange that might reduce the general Zimbabwean preference for pulling everything out of the bank account on payday.

This kind of worked, actually – because there is now a shortage of bond notes, which trade at a premium to bank money. So people adopted them.

However, it didn’t solve the real problem.

Fiscal Deficits, and how to fund them

The big problem here is that the Zimbabwean government is running a fiscal deficit. That is: it’s spending more money than it collects in revenue.

And it has funded this deficit by:

- Issuing Treasury Bills to the bank sector (which is a form of money creation);

- Transferring the loan proceeds into the bank accounts of civil servants; and then

- Allowing those loans to be cashed out for real money.

This is what is forcing the disparity between the markets for USD cash, bond notes and bank money to widen at exponential rates.

And the borrowing is escalating:

- In March 2016, there were about $2.8 billion of outstanding treasury bills.

- In March 2017, there were over $4 billion of them (these figures are taken from the National Treasury quarterly bulletin, Q1 2017 – the last one we’ve seen).

- And in 2017, the projected budget deficit is expected to be double what it was last year.

- So expect the current TB issuance to be floating up near $5 billion.

These are staggering increases in government borrowing. And it’s coming out of bank accounts.

If hyperinflation is a tax on cash balances, and the government is effectively confiscating the money in people’s bank accounts, then the Zimbabwe Hyperinflation is back for round 2.

All our fears are already fully realised.

Zimbabwe Hyperinflation 2.0

Here is the stock market, which is often the most ‘live’ indicator of what people are doing with their money:

What we are seeing is the panicked purchasing of people who do not want to hold their bank balances. And because they can’t withdraw cash, it goes into the stock market. This, after all, is not Zimbabwe’s first rodeo.

And when even the Reserve Bank governor, typically circumspect on political issues, says things like:

“The second creation of money is through the Ministry of Finance by providing Treasury Bills. When the ministry [of Finance] finances the government there will be an overdraft by the RBZ. It means there will be money creation. […]. Those dollars are not backed by foreign currency because people who are exporting are independent from those creating the local dollars. When minister Chinamasa is paying civil servants, say about $20 million above his revenue in a month, that $20 million has nothing do to with exports coming in the country. They are independent. The idea is we need to manage them now.”

You know it’s for real.

Comments

16 responses

To long and unrelated jammed in ideas for one which is suppose to look from technical point. No coherence at all!

The one line that summarises it is”Just reflect on that for a moment. Here is this unwanted paper currency – one that attracted protests and widespread rejection – and it’s worth more than the money that people have in their bank accounts.”

So, TheBond Notes are a success ! Deal with it

Short attention span, you are used to reading bedtime stories. Looks like the word ‘researched article’ is foreign to you. Great article.

Short attention span, you are used to reading bedtime stories. Looks like the word ‘researched article’ is foreign to you. Great article.

If setting up a full isp infrastructure from scatch to operational sounds like short bedtime story, then lm happy to continue doing that

Yawn… Article is well researched and well written – nothing incoherent there. The same can’t be said about your comments though.

Cool story about the ISP infrastructure.

Machchip, you need to go back to scholl becasue this is probably the most accurate article about the current situation in Zim. In fact the rate is forecast to reach 150% before Christmas so lets stop lying to ourselves and look at the facts here.

this seems to be a very clear explanation of the current state of affairs. it may be somewhat lengthy but still makes quite a lot of sense. overall a good article

Biti said eat what you kill . They did not take heed of his advice

Haven’t enjoyed an article on Techzim this much in a while, even if I’m non-financially minded and understood less than half of it. Great job!

Finally understand what a nostro account is.

Great article, next time make it shorter

Good effort. You should however explain and give evidence of how the RBZ is forcing banks to buy its treasury bills and how it is forcing banks to hand over the nostro balances.

The

I donot agree with the notion that bond notes were a “success” and therefore their introduction was justified:

FIrstly , the article rightly points out that the REAL problem was that the average (working) zimbo withdraws most if not all the of their income come payday. Which points to a lack of confidence in the banking (financial) system among other things, therefore when you say the bond notes were a “success” you are purporting that the bond notes ushered in some sort of renewed confidence in the banking sector , absolute nonsence. The reasons for the introduction of bond notes , mentioned in the article seem to differ to what the government and monetary authorites articulated when the new notes were rolled out. I remember government assuring the general population that bond notes would “ease the cash crunch” . The assumption that it would discourage “withdrawals” seems ridiculous.

Lastly , i just want to say that , of course the bond notes have more value than the phantom money sitting in our bank accounts for the simple reason that bond notes are cash and in our context they are an alternative to the USA Dollar notes.

Good. But you have left out that the Office of Foreign Asset Control in New York has been penalising local banks under ZIDERA and taking cash from the Nostro account. If you researched as you indicated why was the sanctions aspect conviniently left out.

The other aspect is the fungibility of the bond notes as compared to currency of our neighbours. The bond notes shortages is because of its ability to be traded across borders. The bond notes is a victim of its success unlike the Zimbabwean dollar of pre 2009

Handei tione

2008 yatizhonya zvakare