Sometime last year we wrote about the M-Ledger Android application that had been launched by Safaricom as an “accounting service” for the mobile money service M-Pesa. It was the product of a Kenyan startup that was working with the leading Kenyan mobile network.

Noticing the relevance of such a service for Zimbabweans who use mobile money more than conventional banking channels, a local developer, Gedion Moyo, (he’s the same guy behind the first EcoCash mobile app that was later blocked by Econet) has come up with his own version of a mobile money ledger service.

Called MobiLedger, the Android app which is still in beta, has been placed in the Google Play Store and the apk has also been made available for download from this link. It currently works for EcoCash only, but Moyo says he will be rolling out support for Telecash shortly.

What does the app do exactly?

MobiLedger acts as a mini accounting system for your mobile money account. It keeps track of all your transactions, records the financial history and categorises the different uses of the money in your wallet for a specific period. What you’d have had to thumb through and often reconcile on your own is then presented clearly.

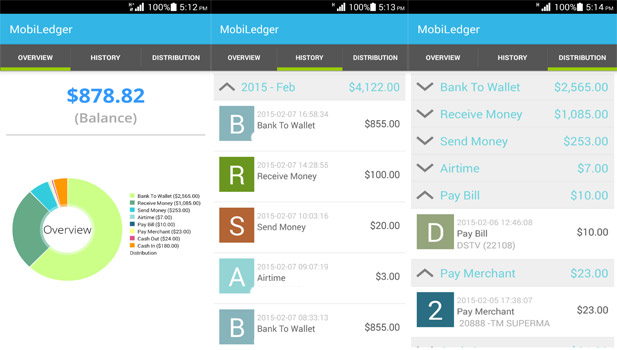

The interface has 3 tabs, Overview, History and Distribution. Overview displays your current mobile money balance as well as a graphical breakdown of the amounts you have spent on the different mobile money services. History offers a track of five months worth of transactions and the Distribution tab displays the related amounts on each service.

Having only had the MobiLedger app for a brief moment I am impressed by the User Interface and functionality presented by the beta version so far. It genuinely makes the monitoring of mobile money movement easier.

Having only had the MobiLedger app for a brief moment I am impressed by the User Interface and functionality presented by the beta version so far. It genuinely makes the monitoring of mobile money movement easier.

For once I don’t have to access my USSD menu or the existing EcoCash app and its prompts to check on my wallet balance or draw up figures for when I sent or received any money or made that DStv payment.

This however felt a bit weird because the price for all this convenience was giving the app unprecedented access to my financial records. It had “privacy violation” sprayed all over it.

If you have embraced mobile money as an alternative to conventional banking transactions, this app will show a very clear paper trail, the sort of information that you wouldn’t want anyone who picks up your phone to go through without any security prompt.

Besides the value this app provides to any mobile money agents who decide to use it, MobiLedger ought to be an asset for traders and informal business people that have turned to their wallets as the main channel for moving money. This, as it turns out, is now a huge market.

The informal market, according to government’s estimates for last year, was handling as much as $7.6 billion of the funds in this country. There’s also the fact that in a survey conducted by the Central bank and Zimbabwean Economic Policy Analysis and Research Unit (ZEPARU), only 24% of small to medium-sized enterprises had opened bank accounts.

The SME transactions are being conducted on mobile money instead. This is something that ought to be considered in further iterations of the app. The value of information and detail should be assigned to these enterprises that rely on mobile money extensively.

These are the same considerations that seem to have been key for the M-Ledger App team when they were working on the solution for M-Pesa. The M-Ledger app has more detail on transactions, agents involved as well as spreads on account activity. These aspects could be added for later versions.

MobiLedger is a great tool for business reconciliation on an entrepreneurship level, and if used correctly it adds weight to the financial literacy objective of mobile money as a financial service tool.

These elements are actually critical for the core market of mobile money services that conduct all transactions in the absence of traditional accounting procedure. Throwing in a financial record helps display where the money is going and hopefully dictate how to plan for where it should be spent next and more importantly, how it should be saved.

Will this app be snapped up by the Mobile Networks?

It’s hard to say whether EcoCash or Telecash would be keen on ploughing money into an existing app. We do not have Silicon Valley acquisitions in these here parts, no matter how relevant a service might appear to be.

What will likely occur is a re-creation of the same service from these mobile networks. It has happened before and now that Econet, as an example, has a core team of development talent, apps like this are hardly as difficult to come up with as they used to be a while ago.

What are your thoughts on this app? What do you think needs to be added to give it a better feel?

Comments

27 responses

I am assuming the app captures the SMS then parses through the SMS and garners the relevant information? If not how does this ledger work seeing as Ecocash only gives the last three transactions.

Dont know much about app permissions on Google Play but this app does request for access to SMS/MMS so I guess that could be where it gets the information from. Any other source would frankly freak me out. Also, I doudbt if Econet would allow any other types of access

Am curious: where does the app access all these data from?

From those SMSes that u get each time u do an ecocash transaction.

Cool. The innovation is in reading about MLedger, seeing its applicability to zim and getting on with it. Well done old chap.

excellent!!!

will this app be available for windows phone??

Yes, of course 🙂 soon

4 stars for local innovation !! incredibly easy to use and useful database of information !!

Thanks mate 🙂

You should have been with the hubs Moyo.

That’s the sad part . Econet won’t support him they will recreate it indoors. it’s so disheartening

true dat.econet magororo.vanoba too bad

i foresee this going far.. seeing that he is now working for Liquid 😉

Ok. Let them transfer him to their sysdev team then.

How would you want Econet to support him?

Is there an option for this on symbian phones?

Great app indeed. M loving it!

Im running Lolipop on my s4 and the app keeps crashing. Is it compatible with Android 5.0.1??? Great app though!!!!!!!!!!!!

@Castro, download the latest app (version 0.0.8) from http://www.mobiledger.com/app.apk, It should fix the crashing on Kitkat and Lollipop. Let me know in the comments if you still experience the crashing after that update

Strive Masiyiwa writes a lot about stirring creativity and innovation in people. It would be nice to see Econet doing what its founding founder preaches by supporting this guy not to steal his idea or shut him out like they did on his first app

There are a couple of things you are missing here:

1. An idea is an idea, Econet would only be doing wrong if they stole his source code and used it for their own purposes.

2. You want Econet to support this guy, I interpret it as you want them to buy this app. Now, why would they buy an app when they can develop one in house? Maybe I misinterpreted you, what do you mean by “support”

3. Strive is the founder and has his own principles, but Econet is a public company and has many other shareholders(some of them Muslims e.t.c). The purpose of a company is to make money and not to abide by some religious principles

no we are saying strive always talks about innovation but when someone comes up with one instead of econet engaging the guy even on a consultant basis they shut downhis stuff. and you wonder why zim it goes nowhere. google grew because it innovated to the extent that it can give away it services for free or as close as free as it can. india does the same.

#sadstateiofzimit

Good app, I am enjoying it-has enabled me to track my income and expenses. woow, it now gives me discipline hey.

On another level, this one will get me into trouble with my wife, lol

lol, the latest version (0.0.9) now has a security layer, unless you share your pin with someone, they wont be able to see your data 🙂

Great app but it’s not about Econet not supporting him but sir you should copyright work