I am excited and disappointed at the news that EcoCash has finally released the EcoCash app. Excited because it was long overdue and this could be the much developer touted API.

I am excited and disappointed at the news that EcoCash has finally released the EcoCash app. Excited because it was long overdue and this could be the much developer touted API.

Much to my disappointed is the calibre of application they chose to release. The application is a simple UI onto which you capture all the details you would normally capture at every *151# session response. The app then proceeds with the transaction by dialling the long USSD all at once and completes the transaction by a USSD prompt for user authentication. Simply put it is a USSD dialler that replaces the multiple back – and – forth capture and dial USSD sessions with a single step session.

Debatably, EcoCash App is one of Econet’s not-so-innovative products and it seriously deviates from the brand vivacity that they have set for themselves with previous offerings. I personally had expected exceptional standards, an application in the likes of Western Union or FNB App. This of course in the absence of an EcoCash App hackathon where developers could have come up with numerous alternatives over a three day marathon.

I say debatably because there must be business sense at EcoCash that supports perpetuating USSD centred services as opposed to internet based and USSD based equally, possibly for the reason that Zimbabwe has an internet penetration of less than 40%. This line of thinking is itself irrational against a backdrop reality that there is a very high influx of affordable devices from various initiatives that include Econet’s own device promotions and other low cost brands such as G-Tel , Karbonn and Astro available on credit terms.

Interesting to note, in fact that over 98% of the penetration refers to internet accessed through mobile phones and devices (GPRS/EDGE/2G/3G/HSDP). The inevitable truth is that in the short to medium term, there will be more than 50% internet penetration, via smartphones. Which then leaves us wondering why Econet had to release a “casual” app whereas it could have provided two releases, one in the manner they deed and another for the more than novice smartphone user if for nothing else but to maintain their rep.

Five obvious improvements

First of all, USSD is no longer the way to go. Yes, in Zimbabwe you will serve a large percentage of mobile phone users. That’s fair and fine but worldwide, considering that EcoCash is seeking to grow global with EcoCash Diaspora shortly, you would then expect that there is an EcoCash App version that caters for the more data mature markets.

First of all, USSD is no longer the way to go. Yes, in Zimbabwe you will serve a large percentage of mobile phone users. That’s fair and fine but worldwide, considering that EcoCash is seeking to grow global with EcoCash Diaspora shortly, you would then expect that there is an EcoCash App version that caters for the more data mature markets.

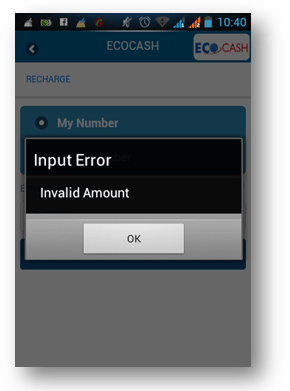

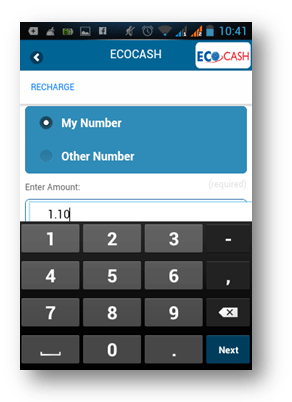

Secondly (If anyone else has noticed) the application does not allow cents. Trying to buy airtime that is not a whole number returns an “invalid input” error. I suspect this is an oversight by their pilot product test team and they need to fix this.

Thirdly the “Next” button does not work after you input your details. You will have to escape from the keyboard screen back to the main application then hit proceed. There is no command level integration between the native keyboard and the app other than data capture.

Fourth, EcoCash needs to add a merchant list and an agent list from which to select the merchant to be paid rather than type in the merchant code. I know many consumers face the same problem of searching for the MultiChoice / DSTv biller code each time they want to pay for Satellite. While on that subject, they need to educate consumers on the difference between an agent code, biller code and merchant code… what a headache.

Fourth, EcoCash needs to add a merchant list and an agent list from which to select the merchant to be paid rather than type in the merchant code. I know many consumers face the same problem of searching for the MultiChoice / DSTv biller code each time they want to pay for Satellite. While on that subject, they need to educate consumers on the difference between an agent code, biller code and merchant code… what a headache.

Fifth, EcoCash needs to add capacity to save recurrent recipients; for example to add vCards for Merchants so they are added to an address book. From here I can then pay the merchant or recipient from a list or from my contacts.

Still no API

Coincidentally this matter reignites anxiety over the contentious API and whether or not the release of this application could be good signs that the EcoCash API is coming soon. As more and more consumers move to higher data consumption, more services and needs are going to be identified. These are not as generic as the “Eco” family of products to be offered only by EcoCash. Addressing some specifics from business to business requires going through a payment engine of some sort.

With the advances they have made in MMT, you would think EcoCash would be at the forefront creating a conducive and enabling environment for interoperability, perhaps not with banks but at least with other players. The added EcoCash traffic should be more than a bonus to them as it not only increases awareness but also identifies more ways in which EcoCash becomes relevant, entrenching itself as an everyday tool. It is not sufficient for them to lay a cobweb of optic fibre cables across the continent and forget to create peripheral lures to excite chatter around that same web.

Denying, delaying or withholding the API could seem trivial to EcoCash possibly considering their projections of demand from services requiring API connection viz-a-viz EcoCash’s own pace of and stage in development. However, it could also be reckless on EcoCash’s part as they stand to lose should the current booming mobile money ecosystem and start-ups find an alternative gateway in the form of Telecash or One wallet?

Why is Econet refusing to avail an API?

- Is Econet capable of developing an API?That sounds like a silly question to ask especially considering this is a multinational company with enough financial muscle to purchase and implement mobile money services from Mahindra Comviva and employ some very adept developers. But this question is justified in the sense that with all of Econet’s might, they had to disable long code USSD because some random developer came up with a Droid app in an afternoon, something Econet had refused or failed to do since launch. When they eventually did release their own “more secure” version, it is no more functionally convenient than a USSD dialler.

A closer look at their technology supplier Mahindra Comviva also sheds a bit of light. From their website, their suites are tailor made to carter for both the banked and unbanked with a more pronounced concentration on USSD services. It could also be possible that as a market penetration offering Mobiquity Money is what Econet settled for. It would seem that this platform only provides the infrastructural ability to offer MMT.

Even in Zimbabwe the core function of MNOs is purely to provide infrastructure. Under normal circumstances VAS companies would then receive an API connection to offer various services. Peculiar to Econet is the fact that they not only formed the EcoCash VAS as an appendage to evade the legal restriction to the monopolistic arrangement where they would offer VAS, they are in fact in the habit of conglomerating all services surrounding Econet including the buyout of TN to Steward Bank and ZOL through Liquid Telecom.

This tendency then crowds out any other players. We will get the API and we will only get it when EcoCash is in the same position to offer the most profitable VAS as any start-up today. In which case again anyone’s internet payments for example will offer no competition with the one from EcoCash whether by pricing or by flexibility.

Supposing they purely depend on the bouquet of Mobiquity Money options, they would then be faced with either an extra cost in the development of interconnectivity gateways to offer other services or increase licencing costs to enable such functionality from Mahindra.

- Is it Hardware?

Could it be issues to do with hardware capacity where Econet says we cannot open a floodgate of traffic that we have not yet provisioned for (security, processing power, gateway administration etc.)? Most likely not, in which case the API question still stands? I can think of half a dozen VAS applications that are clamouring on Econet’s door right now to be connected.The likes of Pay4App, Astro Store, Zimswitch Shared Service, Zimbo Kitchen, TechZim Store, Khayashopping, and Card-to-Mobile services. If all of these were to be connected to the gateway at once, there could open floodgates to traffic that had not been anticipated. That is why one would then need to apply for connectivity stating uptake projections and all the other technicalities of a business case.

- Is it an administration issue?

Could it be that they have limited resources in as far as actually administering the API? Come to think of it, there is the legal side which entails making sure that all members conform to rules, regulations, standards and statutory requirements. There is the standard security certification, there is the business case or model to scrutinise, there is the aspect of guarding against facilitating money laundering, developers from both ends meeting and so forth. This could be a division on its own and it may need more time to setup.If the above is true I would propose; to Econet that they expedite the formation of self-regulating VAS society in the likes of WASPA and dishes out the work to the VAS providers themselves, including sponsoring the necessary hardware and the policing exercise. This is a topic that has been advocated for before here

Whatever the issue is, EcoCash, and I suppose TeleCash should realise that they are doing the nation’s ICT development a disservice. They are not only stunting the growth of start-ups and established businesses but they are also denying consumers solutions that are required on a day to day basis. They are also party to the repudiation of the ideology of financial inclusion which they themselves started off preaching about especially in electronic and mobile commerce specifically and ICT in general.

Comments

14 responses

Disclaimer: I read Techzim and have followed them from the single digit likes/followers days, and advocate for them to the extent that people actually think I’m on the team. So read my comment with an optimistic tone.

Now that being said. As has been said here before we cannot push telecomms companies to work on APIs, Safaricom at their scale DO NOT HAVE an official API and our young mobile money providers cue that up as sign there isn’t much room for business. Also as was put by another gentleman in one of (y)our constant bashing we must remember that at the end of the day these are businesses started for money, don’t buy the manifesto crap. They want money in THEIR pockets when they put ANYTHING out there on market. And they want BIG money while they’re at it. I spoke to the EcoCash leads once and commented on a previous post about this, they said that (me paraphrasing) while they are excited about the possibilities of an API the higher ups are simply not moved by a project that will cost more to build than the profit it will bring them within 6 months of launching.

Which is (even though I punch myself for backing this) a true saying. How many local websites right now are making SOO much money that an EcoCash API will make EcoCash millions and millions? Oh, crickets eh? Yes yes your argument is right I make it also: if we build the API, the eCommerce startups will come. But you see telecomms companies in Africa (most) are not “startups”. They don’t chart new markets, they wait first for the need for a product or service to be big and in their faces so that when they launch it’s an all-out war with amazing returns within the first few months. They don’t bank on the future.

I feel bad for commenting yet again on this topic, some of us had decided in a thread to stop the repetition. Maybe the new (great) authors are yet to fully sync with the community. People are tired of going over and over this issue which is not just Econet’s problem, but something on the continental level. Techies hate complaining about things which they don’t have the power to change, or things for which their opinion is just “talk” and the local people you quoted in this post are doing what techies should – to stop whining and instead work with what they have. Complaining is good because of course it makes clear that there is a problem, but when it becomes recurring rhetoric then it’s a sore that can drive away the hungry-mind community.

One guy at a recent tech event came to me while I was shamelessly on your homepage scouring for my next good read and said “Oh I see you’re reading Rantzim again”. I’m still trying to decipher the entire meaning of that phrase.

Bu great review of the EcoCash Android app, and looking forward to meeting at GetSocial. Anyone here coming as well? I’d love to meet the community in person again like the good ol times when we had those techizim braais

Thanks for the feedback. I’m chuckling to myself wondering who you are coz you can only be one of a very small subset of people.

I didn’t see the rant in the article. I saw someone that’s exploring the reasons there’s no API much the same way you have in your comment -> business numbers (USSD vs smartphone count), capacity at the mobile operators and therefore the cost to produce an API, security & regulation…

He actually suggests a solution; a VAS startups collective… which yes, we have suggested before. The VAS people haven’t done much and the operators are not in a hurry to have one….

Writer has an optimistic outlook on smartphone numbers going up rapidly, i guess in much the same way the internet numbers are right now.

Is ‘not banking on the future’ itself not a problem? Surely there should be some kind of exploration of where cheese will be in the future, instead of just waiting for the Europeans, Indians & Chinese to do it for us and charge an arm and leg for it. it may not be allocated as much resource as the million dollar stuff. doesn’t this just become a gold rush then?

The point of an API is not web eCommerce where we then just count a couple of shopping cart sites and say the size of market is too small.

It’s about creating a VAS community that will produce solutions that you and I can’t imagine right now. whether it’s web eCommerce, smartphone apps, feature phone apps, in-store apps whatever. The reason WhatsApp is significant enough for them to create WhatsApp bundles is the same reason they should open up and encourage the market to innovate…

this, I hope, is not a rant. and thanks again for the feedback!

You have put my thoughts on paper .

It seems like a web app/phonegap app which sends href short codes to the dialer. Key functions still require ussd dialiing rather than everything being done in-app, as they ideally would be. As a result it might actually be faster to do things the old ussd way, let me see.

This app could be so much more useful for me if

1. It accepted cents. Given that their minimum transaction amout is 50cents (to accommodate kombis) it could be an oversight in designing the app

2. I unsuccessfully tried to pay my DStv on it last night. It looks like a DStv payment is a BILL payment as opposed to a “pay merchant” type of transaction which the app cannot handle.

Until a better app comes out, lets hope that they can fix this soon.

Dear @kabweza:disqus

Would it be too much to get a walk-through video from you guys?

Some of us are outside the country and so have no access to the functionality of the app but I am sure with a video one can easily grasp what’s going on and perhaps figure out one or two workarounds.

Cheers,

Not too much! we’ll see what we can do.

Where is the credit link for the EcoCash image used ?

This articles oozes of boredom and is the type of article we expect in a high school school magazine.

We used 3 images,. the first is an EcoCash App icon. That belongs to Econet and the image itself says so. The others are screenshots which we took.

Thought there were quite many payment options in the universe and any serious developer could use any of those rather than expect to be led by an MNO, whose primary purpose is actually communication and not payments. These imagined developers out there, for goodness sake must start doing something – there are many, many web sites today that take payments and did not need to wait for MNO’s to create an API for them. Needed is a mindset shift that sees and exploits opportunities rather than this wait for MNO game.

No one is waiting for the MNO. People just pointing out that there could be much more value if they came to the party. Local developers have already produced workarounds.

This used to be the case, yes. EcoCash is sign enough that they have entered an arena they were not in before. Econet is a payments & switching company, much like ZimSwitch, Zimpost.

Have you guys ever approached Econet to seek their position on the API/app issue?

Worst app i hv ever used.

Well said, really true, I had almost similar views and my friends thought otherwise…..